The great thing about a money order is that it’s prepaid and a secure alternative to cash. This means that you don’t have to wait for the funds to clear from your bank account like you would with personal cheques. The money is taken before the money order is cashed, as well as any service fees. The amount you choose to send will determine how much your service fees are.

Where to Get Money Orders

In Canada, there are quite a few different places where you can get money orders. While you can get them at your traditional financial institutions such as banks or credit unions, you can also get them at the post office and money transfer locations like Western Union. Some convenience stores, grocery stores and cheque-cashing places also sell money orders.

Process of Money Orders Based on Location

How you purchase or cash a money order is based on location. Each location has a different process and charges different fees. Let’s take a look at how it works.

Scotiabank

With the growing popularity of e-transfers and international transfers, not as many Canadians are using money orders as they used to. That said, there are still some situations when they would come in handy. In this case, you would go to Scotiabank directly and purchase a money order. While there is no fee listed for purchasing a money order at Scotiabank, the standard fee is between $9 and $10.

CIBC

With CIBC, you can also purchase a money order, even though they’re less popular. In order to purchase a money order, the fee is $9.95, no matter what amount you purchase the money order for. This is also the same fee you would pay for a bank draft, which is also available through the bank.

Canada Post

An alternative to purchasing or cashing your money order at a bank is Canada Post. While it doesn’t cost anything to cash a money order with Canada Post when you receive money, it costs $8.50 each to purchase postal money orders. The maximum amount that you can get a money order for with the postal service is $999.99.

When purchasing a money order with Canada Post, you can’t use a credit card to supply the funds. However, you can use a debit card or cash. While the maximum amount per money order is $999.99, you can send up to $3,000. Whether you’re purchasing or cashing in the money order, you do need a government-issued ID. If you’re sending cash up to $3,000 to one person or $10,000 or more when you purchase multiple money orders, then the transactions will be recorded.

Western Union

With Western Union, you can purchase or redeem a money order for whatever you need. Essentially, a money order is a prepaid cheque and can be purchased through any Western Union location. The cost of the money order is based on how much is being sent. To redeem a money order, the cost is $5 for amounts under $100 and $15 for amounts over $100.

How to Fill Out A Money Order

When you purchase a money order, since it is a safe alternative with security features in place, you’re going to have to fill out some information to verify who you are as the sender and to verify the correct person receives the funds. The information you need to supply includes the following:

- Payee’s information

- Senders information

- Amount

When filling out a money order, it’s important that the information is correct. You want to verify that the recipient’s address and name are spelt correctly, as well as your own. The correct amount should also be put on the form. You, as the sender, need to provide a valid government ID when you purchase the order, and the person receiving the funds will need to provide a valid ID as well in order to cash it.

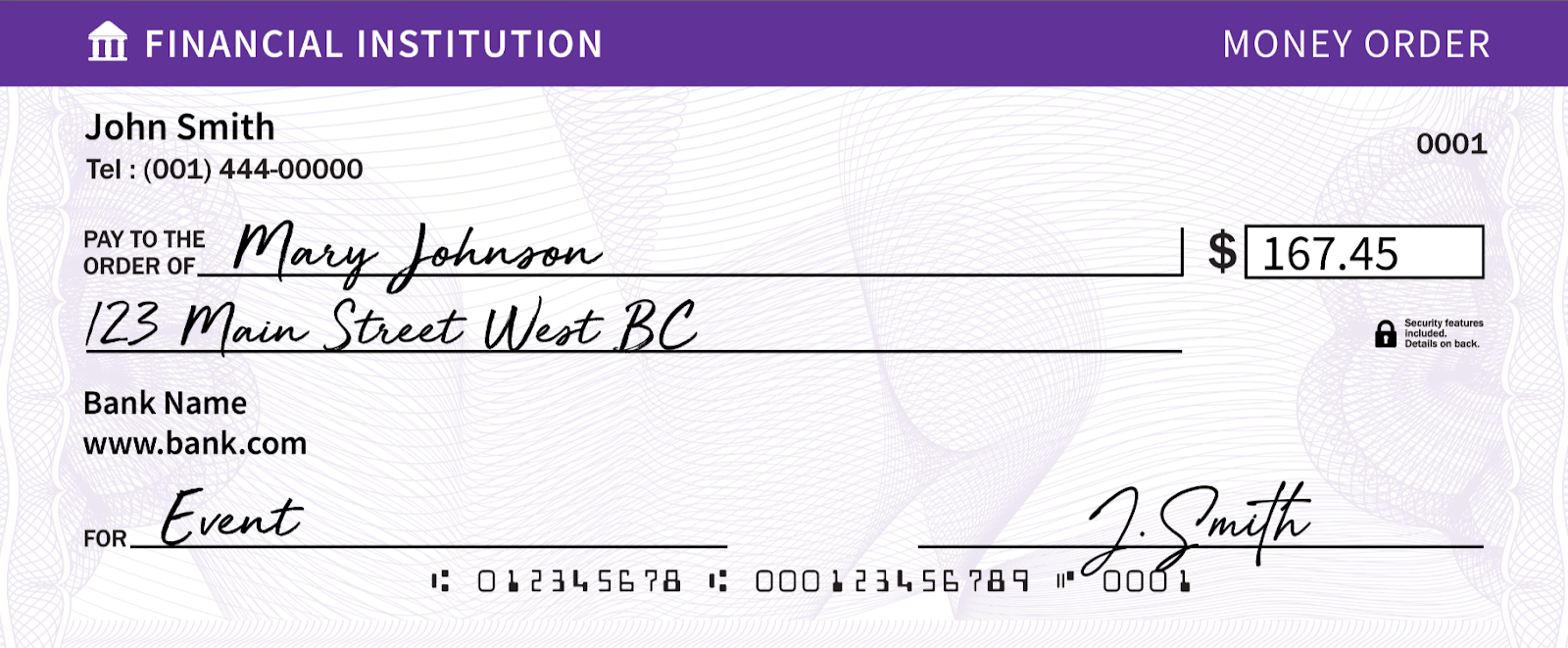

Example of A Money Order

Similar to a cheque, a money order is a piece of paper that is given as a form of payment. The difference is that you pay in advance for a money order. Here’s an example of what a money order looks like.

Money Orders and Expiration Dates

Since money orders are purchased upfront as a secure payment method, they don’t expire. However, depending on how long it takes for them to be cashed, the sender or the payee may be charged service fees. Typically, if they are not cashed within one to three years, service fees will be charged.

Sending a Money Order Online

Due to the fact that money orders are paper documents, they can’ be sent online. However, if you’re looking to send funds online, then that would be in the form of a wire transfer or e-transfer, depending on where the funds are being sent. If you do choose to send money online instead, there are plenty of options available to you. Here are how some of digital payment options work.

Global Transfers

Global transfers are electronic transfers that the bank performs that send money internationally from your bank account to the payee you specify. Depending on your bank account, these transfers may be included. Otherwise, there should be a small fee.

Wire Transfers

Wire transfers are money transfers that are usually done using a third-party service. There are a few that you can use, and each allows you to send money using a credit card, debit or money transfer. The fees for wire transfers depend on the currency that you’re sending, the location and how much you send.

E-Transfers

Interac e-transfers are money transfers that can be sent to anyone with a Canadian bank account and an email address. You can set up a secret question that the payee has to answer to receive the funds, or if they have auto-deposit, the funds will be deposited directly into their bank account.

Pros and Cons of Money Orders

Money orders aren’t as popular as they used to be, but they still have their uses. That said, there are also some downsides to money orders, so let’s take a look.

Pros

There are many cases in which money orders come in handy. These include things like purchasing items or ending money in the mail. They’re ideal for these situations because of the guaranteed funds since it’s paid in full beforehand. Plus, you can track the funds with a tracking number so you know when they’ve been cashed, even if you don’t have a chequing account or savings account. You don’t just have to send domestic money orders; you can also send international money orders.

Cons

Along with the pros of money orders, you also have to consider the cons. When you purchase a money order, there’s always a fee involved. This is usually a standard fee and is not based on the amount. Plus, there’s usually a maximum of $1,000; they aren’t meant to be used for large purchases.

Another thing to consider when sending money with a money order is that many places don’t allow you to use a credit card to purchase them. You have to use cash or a debit card and have enough money to cover the full amount including fees. If you do purchase one at a place that allows you to use a credit card, there’s usually an extra charge involved which adds to how much the money order costs.

Another risk with money orders is money laundering. This means that the money order is purchased with illegitimate funds and turned into legitimate funds. However, if your money order is lost or stolen, ID is still required for them to cash it. You should still report it immediately though in order to prevent fraud from a stolen money order being cash. You should have a serial number that you can report.

Money Orders vs. Cashier’s Cheques

Since there are many different ways you can send money, a money order isn’t the only option for prepaid payment. Another choice is a cashier’s cheque, referred to in Canada as a bank draft or a certified cheque. However, it’s slightly different from a money order.

Unlike a money order, certified cheques have to be purchased at a bank and are typically used for large purchases, meaning one cashier’s cheque or certified cheque can be used instead of several money orders; they also tend to have higher fees. Just like a money order, though, you need to have the exact amount of money you’re putting on the cheque.

You have to go to your bank to request certified cheques. You also need the payee’s information in order to have the cheque addressed to them and certified. The funds you’re sending with the certified cheque are put on hold in your bank account by the bank until the certified cheque is cashed, making it a guaranteed payment. This is different from a money order that’s paid upfront. However, with both paper payment methods, only the person it’s made out to can cash it.

Wrapping Up

Money orders may not be the best form of payment for every situation, but they’re a great idea for those looking to make payments without using cash and for those without bank accounts. Since they can be purchased at many different places, including Western Union locations and Post Offices, you don’t actually need to go to a bank.

The thing to remember about money orders is that they’re usually for less than $1,000. If you’re looking for a method of payment similar to a money order but for a larger dollar amount, then you’re going to want a certified cheque. That said, there are plenty of different ways you can choose to pay bills or send money; money orders are just one of them.