|

|

|

Bank Loans

|

Credit Cards

|

Payday Loans

|

|---|---|---|---|---|

|

Max Amount

|

$35,000

|

$50,000

|

$10,000

|

$1,500

|

|

Interest Rates

From |

9.99%

|

9.99%

|

$19.99%

|

200-450%

|

|

Fully Online Application

|

|

|

|

|

|

Fast Approval

|

|

|

|

|

|

e-Transfer

Delivery |

|

|

|

|

|

|

|---|

|

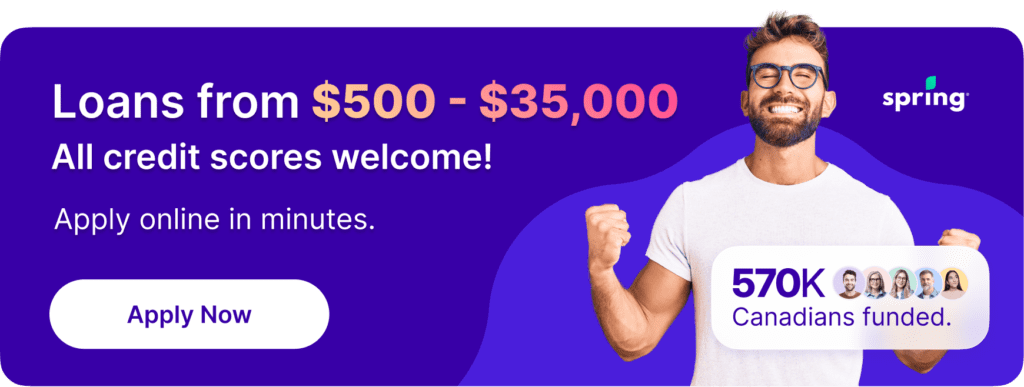

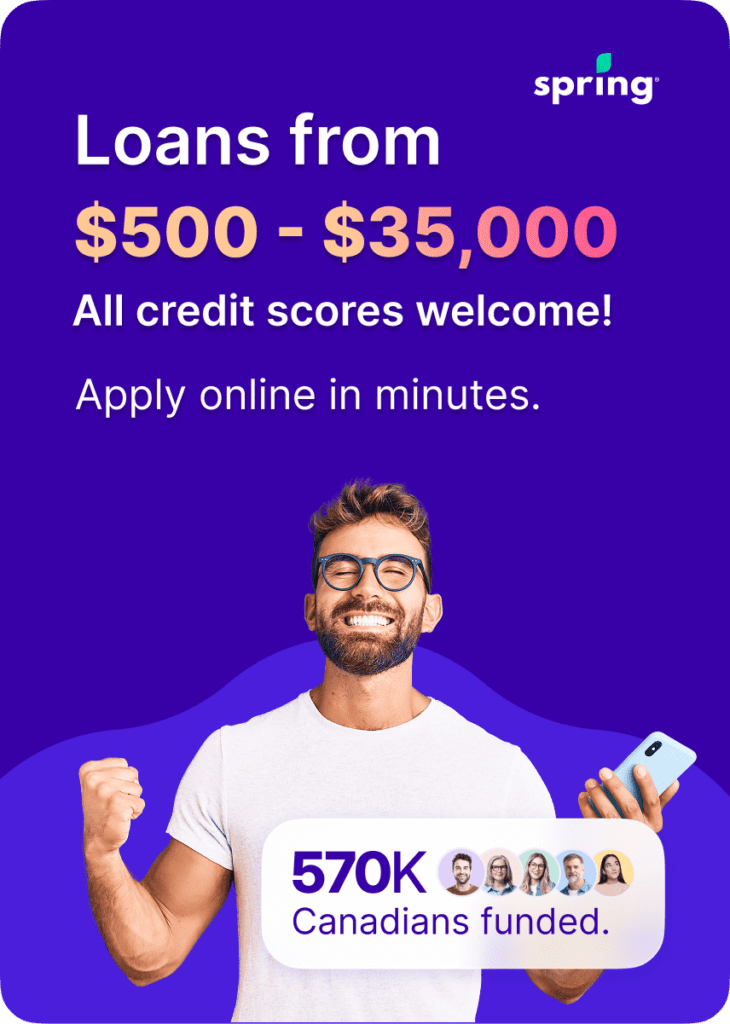

Max Amount

$35,000 |

|

interest Rates From

$9.99% |

|

Fully Online Application

|

|

Approval within

Hours |

|

Same-Day

E-Transfer |

|

Bank Loans

|

|---|

|

Max Amount

$50,000 |

|

interest Rates From

9.99% |

|

Fully Online

Application |

|

Approval within

Hours |

|

Same-Day

E-Transfer |

|

Credit Cards

|

|---|

|

Max Amount

$10,000 |

|

interest Rates From

$19.99% |

|

Fully Online

Application |

|

Approval within

Hours |

|

Same-Day

E-Transfer |

|

Payday Loans

|

|---|

|

Max Amount

$1,500 |

|

interest Rates From

200-450% |

|

Fully Online

Application |

|

Approval within

Hours |

|

Same-Day

E-Transfer |